ISSN 0439-755X

CN 11-1911/B

主办:中国心理学会

中国科学院心理研究所

出版:科学出版社

CN 11-1911/B

主办:中国心理学会

中国科学院心理研究所

出版:科学出版社

心理学报 ›› 2026, Vol. 58 ›› Issue (4): 651-666.doi: 10.3724/SP.J.1041.2026.0651 cstr: 32110.14.2026.0651

马家涛1,2, 李纾1( ), 何贵兵1()

), 何贵兵1()

收稿日期:2025-02-19

发布日期:2026-01-16

出版日期:2026-04-25

通讯作者:

李纾, E-mail: lishu@psych.ac.cn;基金资助:

MA Jia-Tao1,2, LI Shu1(), HE Guibing1()

Received:2025-02-19

Online:2026-01-16

Published:2026-04-25

摘要:

框架效应是违背理性决策公理的稳健现象。本研究旨在检验在损失领域跨时间段决策中是否存在框架效应, 并探讨其对债务置换政策的可能影响。研究发现:(1)对于债务到期日与总量均不变的单一方案, 不同框架显著影响债务人接受程度。相较于高频框架(如周付), 低频框架(如年付)能显著提高债务人的接受程度; (2)对于债务到期日不同但总量恒定的二择一方案, 不同描述框架显著影响债务人偏好。相较于高频框架/常规时间轴, 低频框架/压缩时间轴使债务人更倾向于接受利率高、期限短的初始债务方案。实验观察到的决策偏好符合“图形编辑的齐当别模型” (The Graph-edited Equate-to-differentiate Model)的预测。本研究开启了对损失领域跨时间段决策的理解, 为“时间助推工具箱”提供了新工具, 并为债务置换政策评估和债务管理优化提供了心理科学支撑。

中图分类号:

马家涛, 李纾, 何贵兵. (2026). 损失领域跨时间段决策的框架效应将影响债务置换决策偏好. 心理学报, 58(4), 651-666.

MA Jia-Tao, LI Shu, HE Guibing. (2026). The framing effect of cross-period temporal choice in the loss domain will influence the preference for debt-swapping decisions. Acta Psychologica Sinica, 58(4), 651-666.

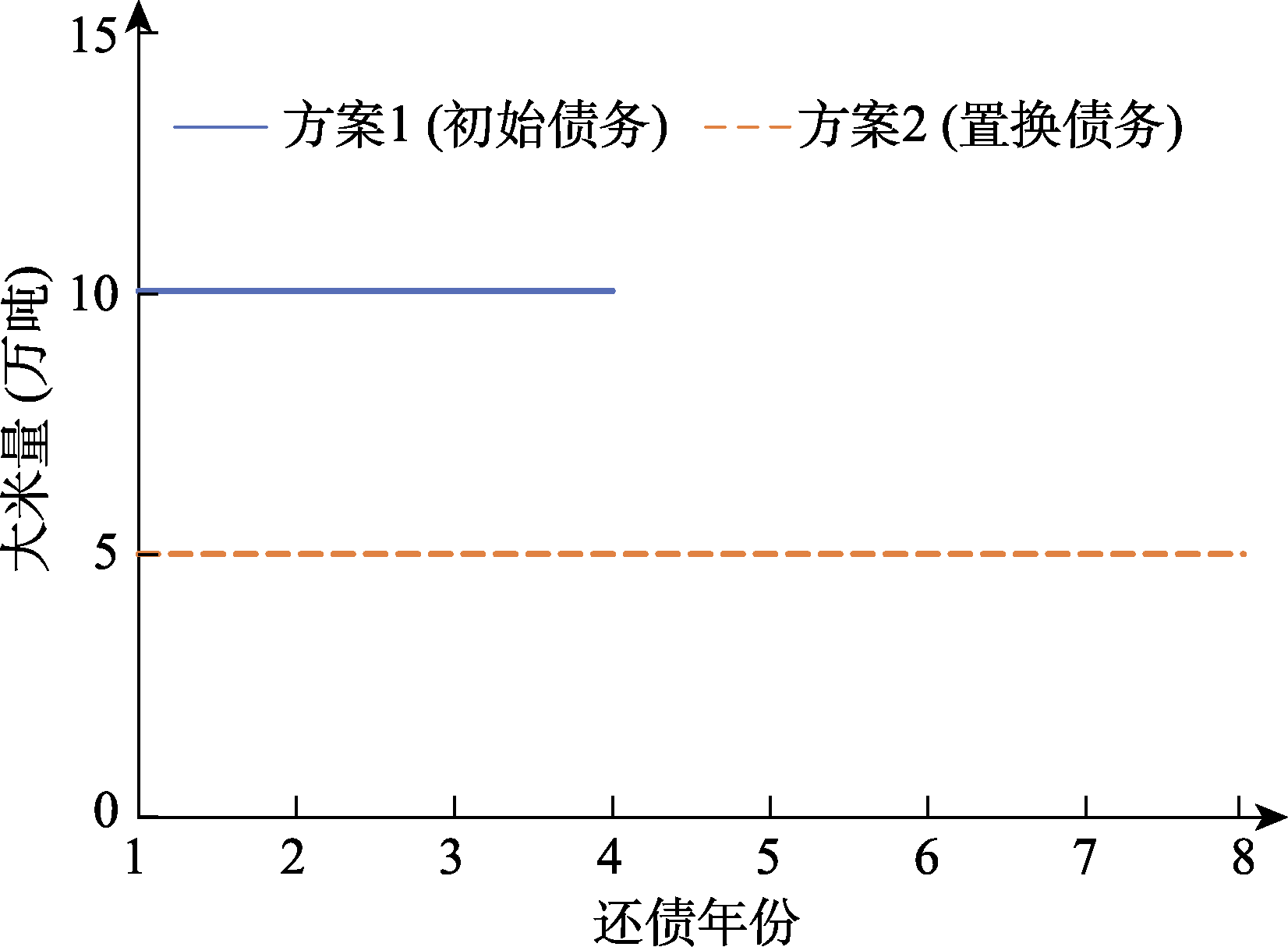

图1 对初始债务和置换债务的图形描述

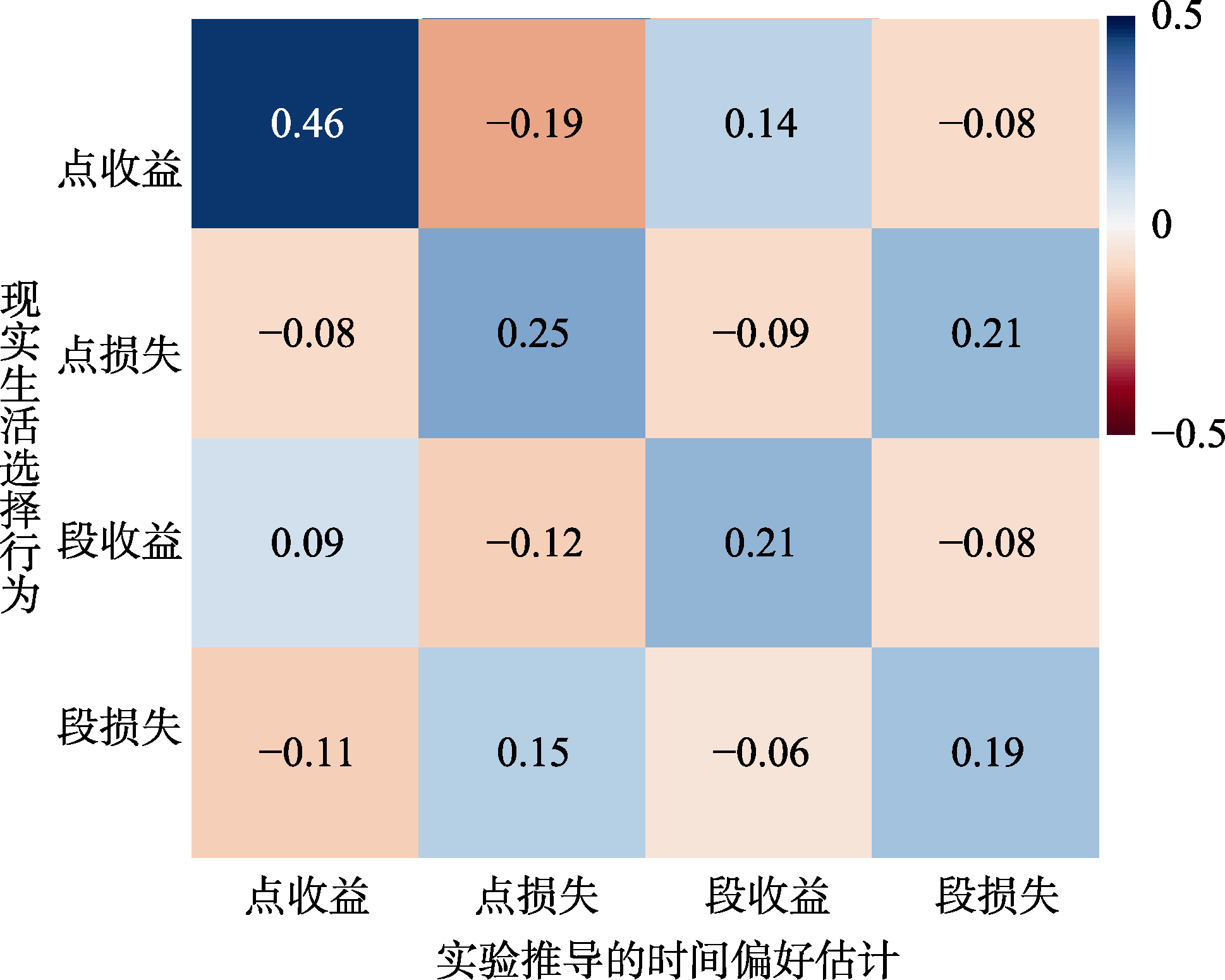

图2 “实验推导的时间偏好估计”与“现实生活选择行为”相关系数矩阵热图 (用马家涛等(2024)实验数据绘制)。鉴于样本量充足(N = 1200), 所有系数在统计上均达显著水平, 图中仅展示系数值(即效应量), 未另行标注显著性。彩图见电子版, 下同。

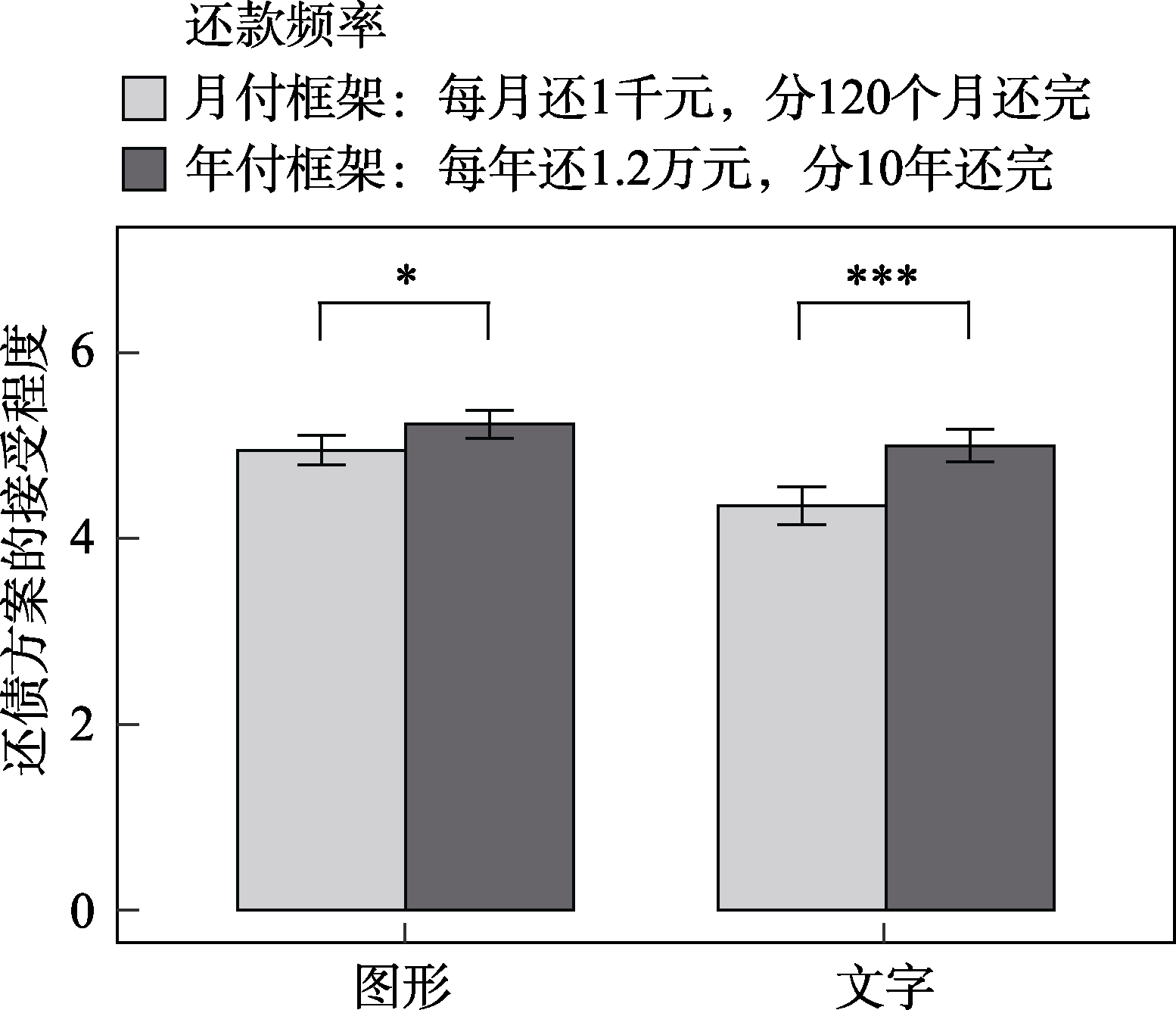

图3 不同呈现形式(文字 vs. 图形)和还款频率(月付 vs. 年付)下对还债方案的接受程度。还款频率越低(年付), 决策者对还债方案的接受程度越高。* p < 0.05; *** p < 0.001

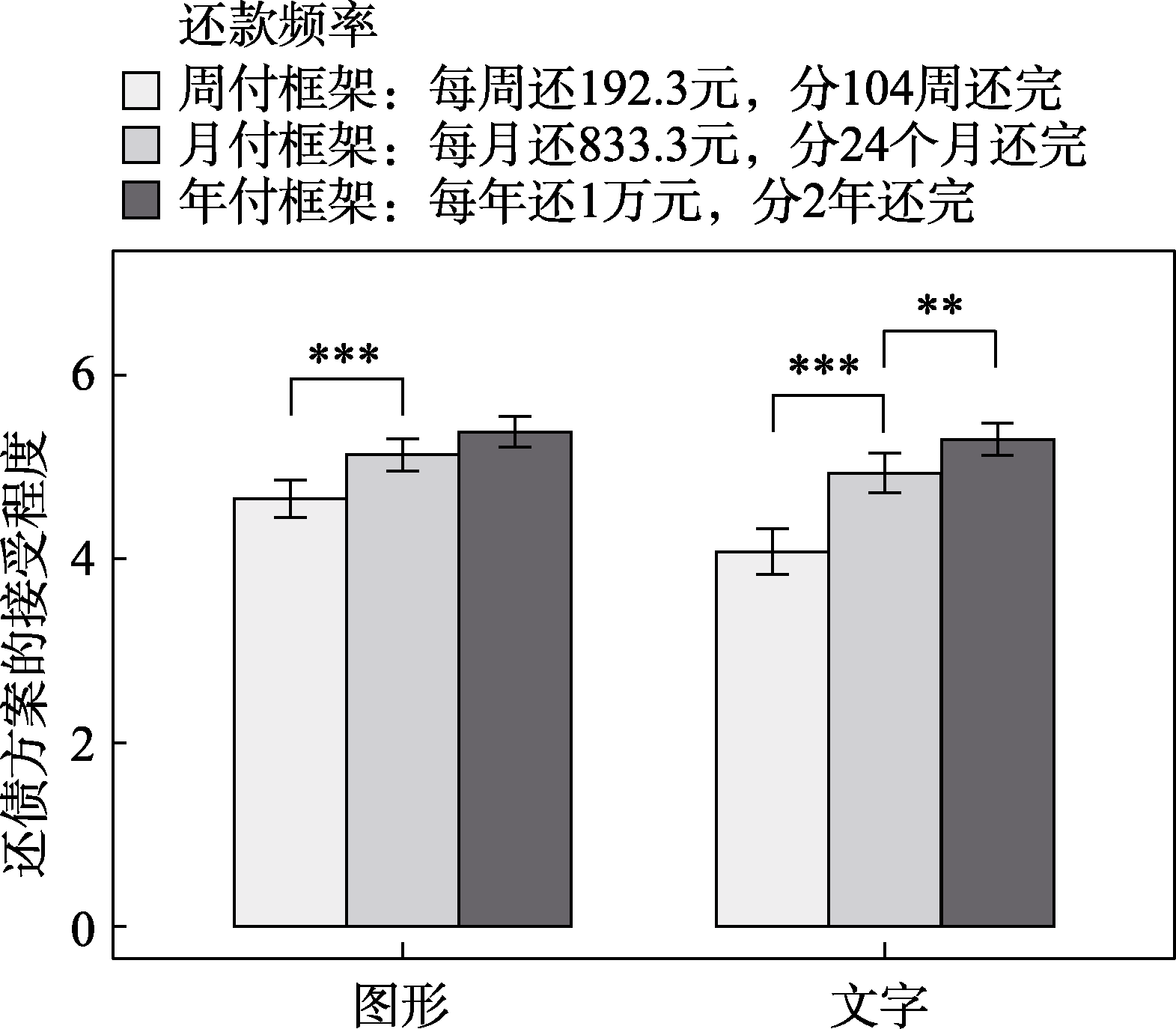

图4 不同呈现形式(图形 vs. 文字)和还款频率(周付 vs. 月付 vs. 年付)下对还债方案的接受程度。随还款频率降低(周付→年付), 决策者对还债方案的接受程度升高。** p < 0.01; *** p < 0.001

图5 月付(a)、年付(b)和压缩(c)框架下的配对债务图形

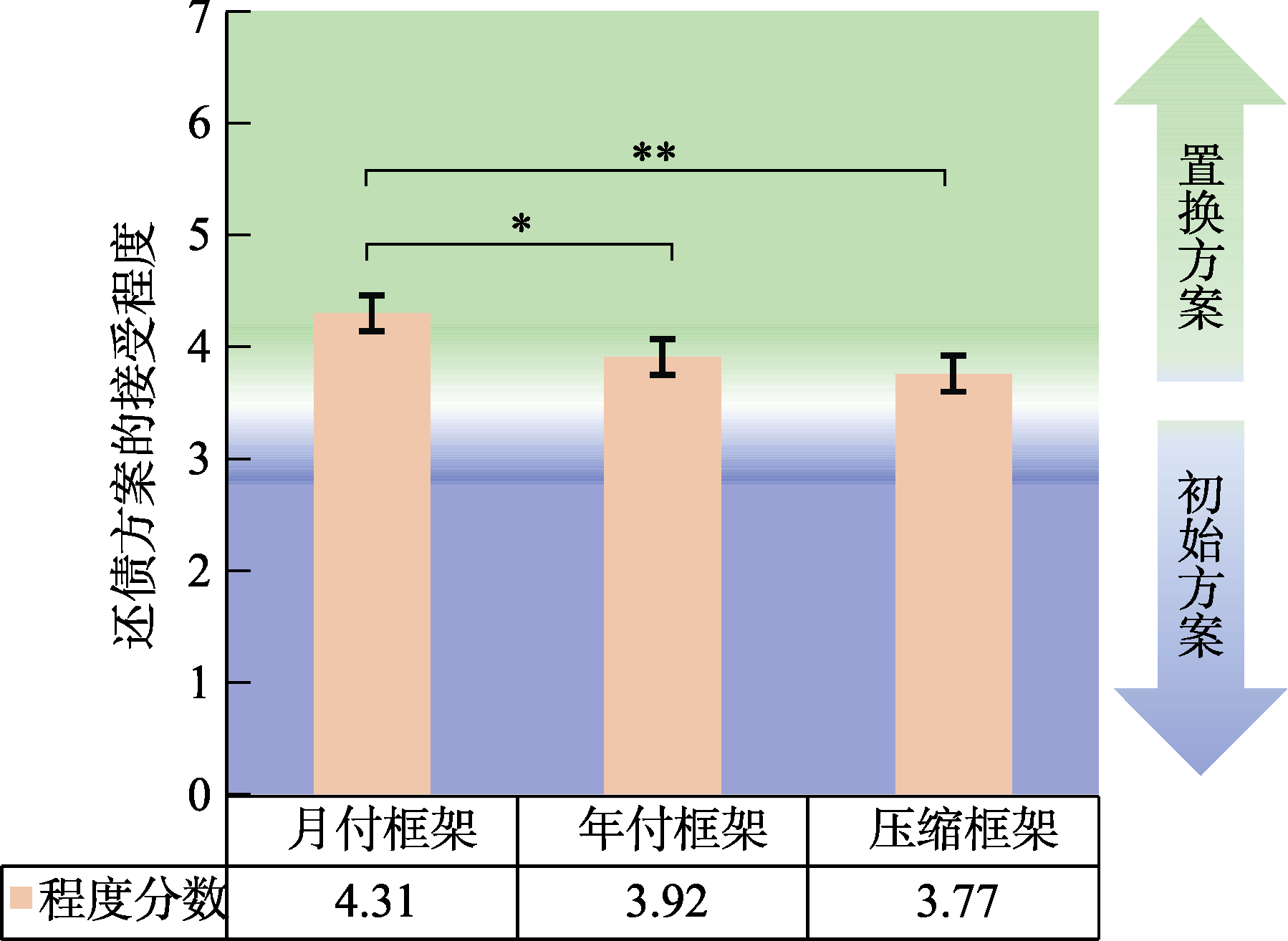

图6 不同框架下对还债方案的接受程度。* p < 0.05; ** p < 0.01

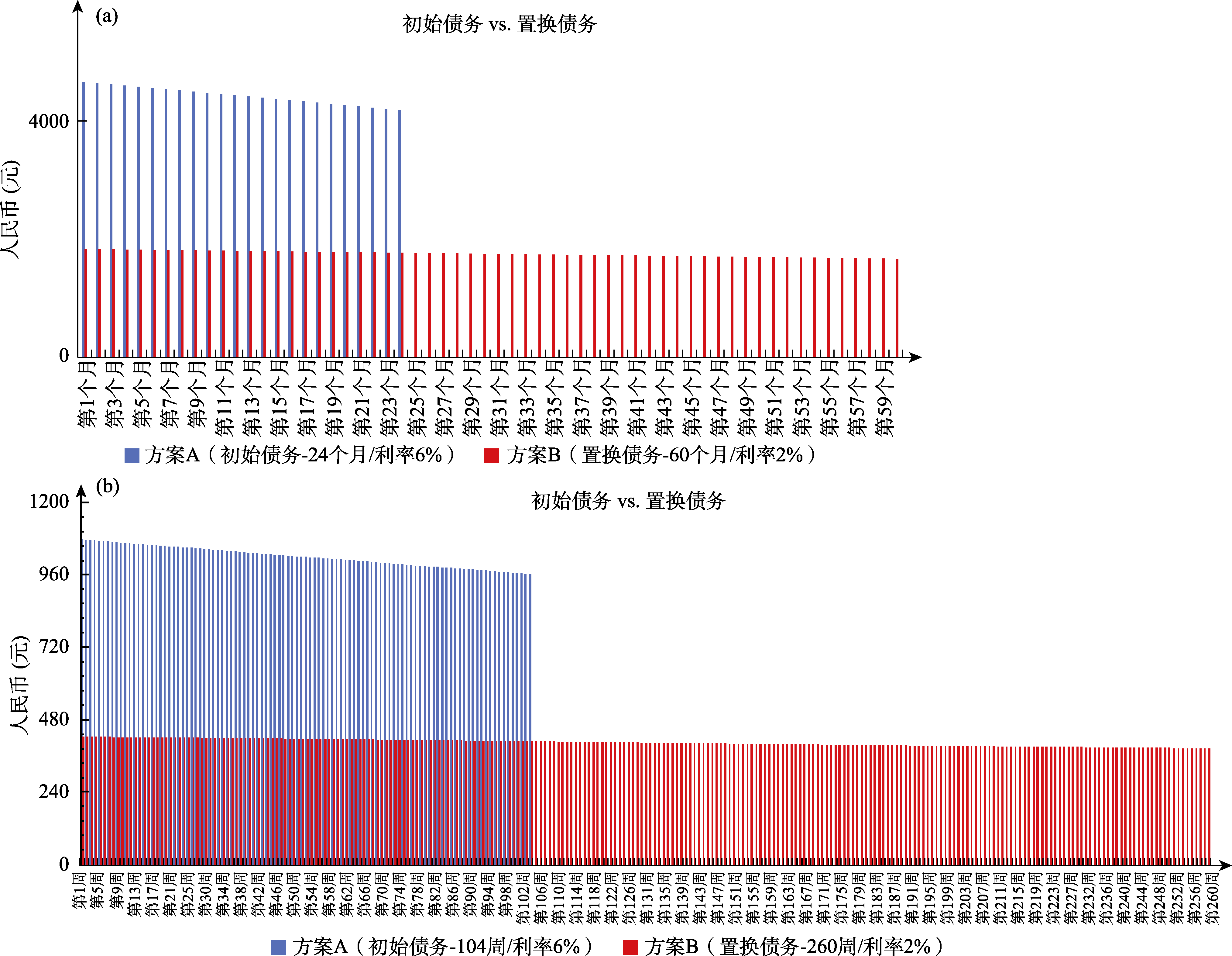

图7 研究2b中的还款频率框架:月付(a)和周付(b)框架下的配对债务图形

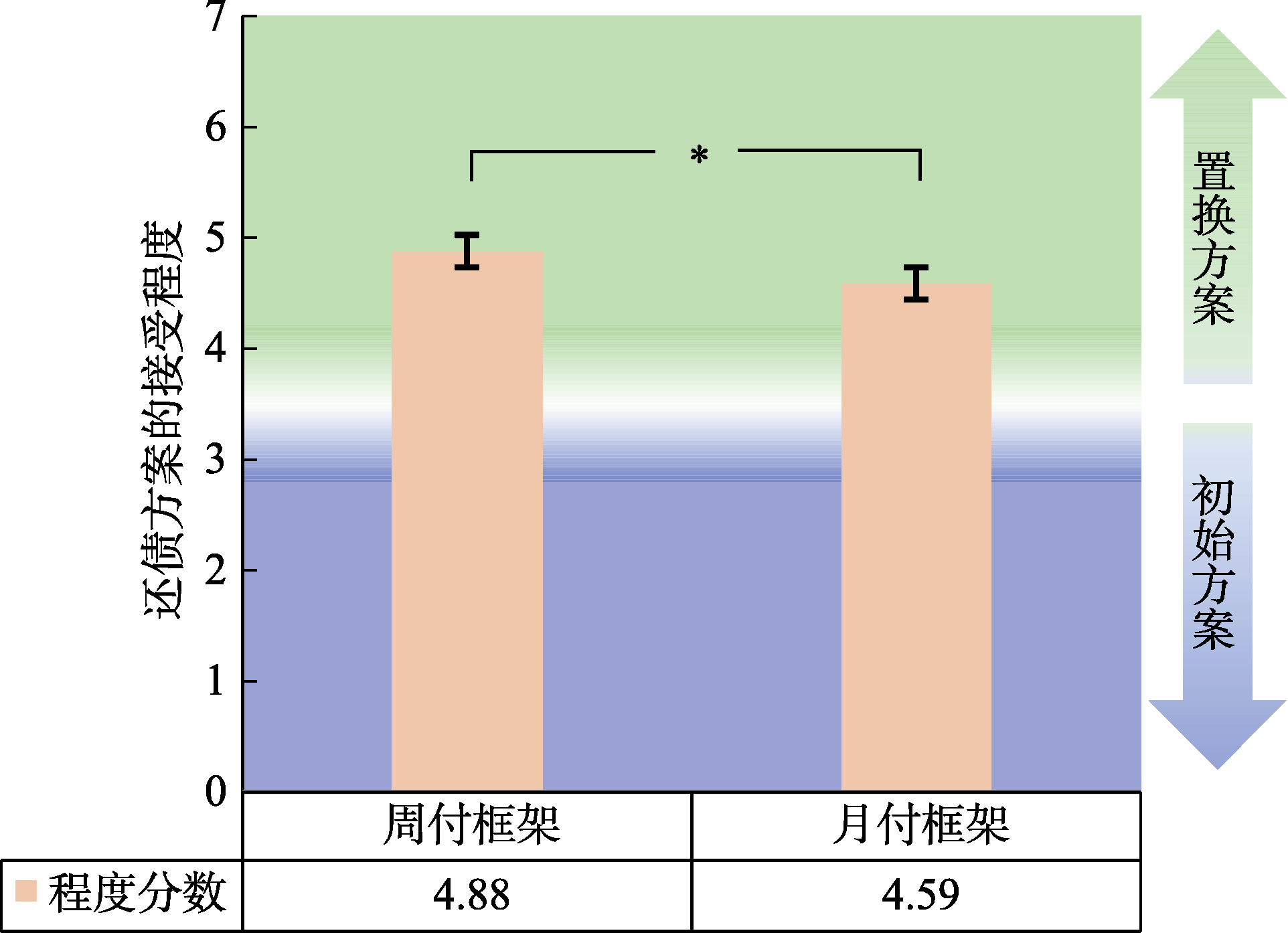

图8 不同框架下对还债方案的接受程度。* p < 0.05

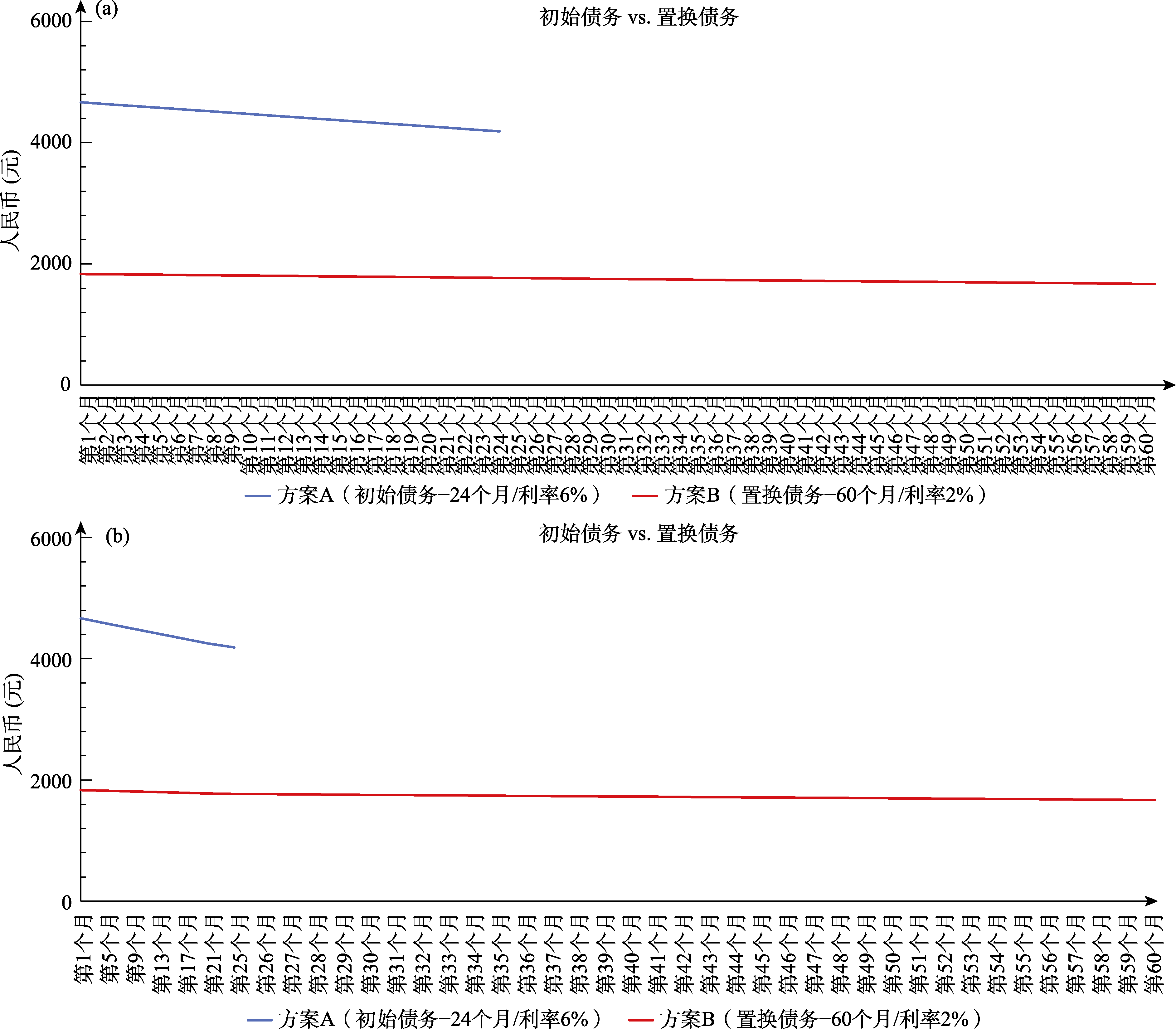

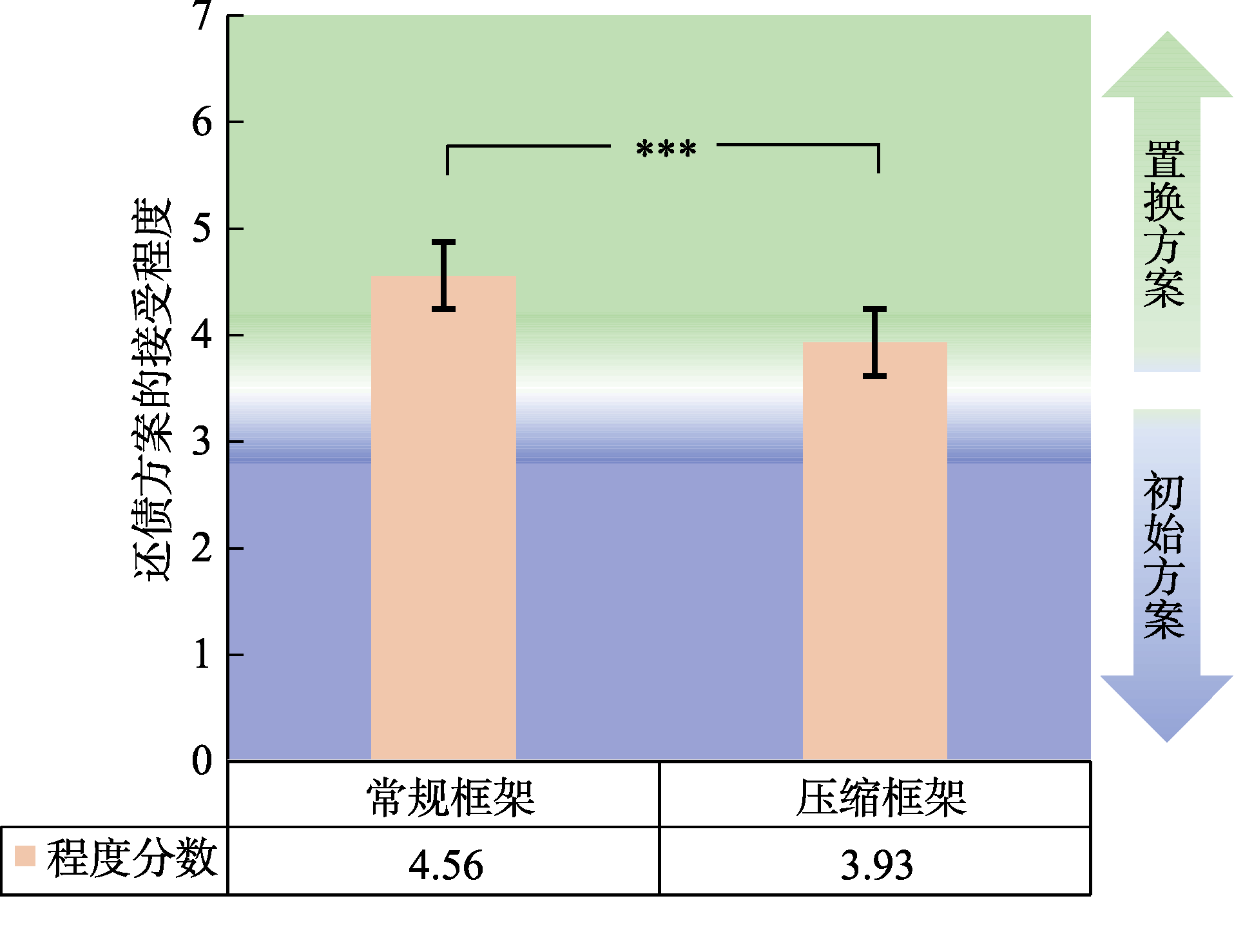

图9 研究2b中的压缩时间轴框架:常规(a)和压缩(b)框架下的配对债务图形

图10 不同框架下的还债方案接受程度。*** p < 0.001

图11 左:用“等距时间框架”表达的美国GDP变化; 右:用“不等距时间框架”表达的世界GDP变化 (来源: https://howmuch.net/)

| 研究 | 方案类型 | 具体方案 | 总额(元) | 计算说明 |

|---|---|---|---|---|

| 研究1a | 年付框架 | 每年还1.2万元, 分10年 | 120, 000 | 1.2万/年×10年 |

| 月付框架 | 每月还1千元, 分120个月 | 120, 000 | 1千/月×120个月 | |

| 研究1b | 年付框架 | 每年还1万元, 分2年 | 20, 000 | 1万/年×2年 |

| 月付框架 | 每月还833.3元, 分24个月 | 19, 999.2 | 833.3元/月×24个月 | |

| 周付框架 | 每周还192.3元, 分104周 | 19, 999.2 | 192.3元/周×104周 | |

| 研究2a | 初始债务 | 利率5%、36个月/3年 | 107, 708 | 单利计算 |

| 置换债务 | 利率2%、84个月/7年 | 112, 750 | 单利计算 | |

| 研究2b-月付频率 | 初始债务 | 利率6%、24个月 | 106, 250 | 单利计算 |

| 置换债务 | 利率2%、60个月 | 105, 080 | 单利计算 | |

| 研究2b-周付频率 | 初始债务 | 利率6%、104周 | 105, 012 | 单利计算 |

| 置换债务 | 利率2%、260周 | 103, 806 | 单利计算 | |

| 研究2b-压缩时间 | 初始债务 | 利率6%、24个月 | 106, 250 | 单利计算 |

| 置换债务 | 利率2%、60个月 | 105, 080 | 单利计算 |

附表2 各研究中债务选项总额及其计算详情

| 研究 | 方案类型 | 具体方案 | 总额(元) | 计算说明 |

|---|---|---|---|---|

| 研究1a | 年付框架 | 每年还1.2万元, 分10年 | 120, 000 | 1.2万/年×10年 |

| 月付框架 | 每月还1千元, 分120个月 | 120, 000 | 1千/月×120个月 | |

| 研究1b | 年付框架 | 每年还1万元, 分2年 | 20, 000 | 1万/年×2年 |

| 月付框架 | 每月还833.3元, 分24个月 | 19, 999.2 | 833.3元/月×24个月 | |

| 周付框架 | 每周还192.3元, 分104周 | 19, 999.2 | 192.3元/周×104周 | |

| 研究2a | 初始债务 | 利率5%、36个月/3年 | 107, 708 | 单利计算 |

| 置换债务 | 利率2%、84个月/7年 | 112, 750 | 单利计算 | |

| 研究2b-月付频率 | 初始债务 | 利率6%、24个月 | 106, 250 | 单利计算 |

| 置换债务 | 利率2%、60个月 | 105, 080 | 单利计算 | |

| 研究2b-周付频率 | 初始债务 | 利率6%、104周 | 105, 012 | 单利计算 |

| 置换债务 | 利率2%、260周 | 103, 806 | 单利计算 | |

| 研究2b-压缩时间 | 初始债务 | 利率6%、24个月 | 106, 250 | 单利计算 |

| 置换债务 | 利率2%、60个月 | 105, 080 | 单利计算 |

| [1] |

Arrow K. J. (1982). Risk perception in psychology and economics. Economic Inquiry, 20(1), 1-9.

doi: 10.1111/ecin.1982.20.issue-1 URL |

| [2] |

Bartels D. M., Li Y., & Bharti S. (2023). How well do laboratory-derived estimates of time preference predict real-world behaviors? Comparisons to four benchmarks. Journal of Experimental Psychology: General, 152(9), 2651-2665.

doi: 10.1037/xge0001380 URL |

| [3] | Bonini B., Hadjichristidis C., & Graffeo M. (2018). Green nudging. Acta Psychologica Sinica (心理学报), 50(8), 814-826. |

| [4] | 财政部. (2025). 2025年6月地方政府债券发行和债务余额情况. 财政部官网. 2025-07-30取自 https://yss.mof.gov.cn/zhuantilanmu/dfzgl/sjtj/202507/t20250730_3968958.htm |

| [5] |

Faul F., Erdfelder E., Buchner A., & Lang A. G. (2009). Statistical power analyses using G*Power 3.1: Tests for correlation and regression analyses. Behavior Research Methods, 41(4), 1149-1160.

doi: 10.3758/BRM.41.4.1149 pmid: 19897823 |

| [6] |

Frederick S., Loewenstein G., & O’donoghue T. (2002). Time discounting and time preference: A critical review. Journal of Economic Literature, 40(2), 351-401.

doi: 10.1257/jel.40.2.351 URL |

| [7] |

Geng X., Zhang K., Ma J., Yang H., Chen Z., & Li S. (2023). Blue, rather than red light can nudge employees to choose delayed but larger wage payment. Environment and Behavior, 54(9-10), 1227-1250.

doi: 10.1177/00139165231153160 URL |

| [8] |

Gigerenzer G., & Gaissmaier W. (2011). Heuristic decision making. Annual Review of Psychology, 62(1), 451-482.

doi: 10.1146/psych.2011.62.issue-1 URL |

| [9] |

Gigerenzer G., Luan S., & Liu Y. (2019). Are we truly irrational and almost impossible to educate? Analyzing the scientific evidence behind libertine paternalism. Acta Psychologica Sinica, 51(4), 395-406.

doi: 10.3724/SP.J.1041.2019.00395 |

|

[Gerd Gigerenzer, 栾胜华, 刘永芳. (2019). 人非理性且难教化?论支持自由家长主义的证据. 心理学报, 51(4), 395-406.]

doi: 10.3724/SP.J.1041.2019.00395 |

|

| [10] |

Green L., Fristoe N., & Myerson J. (1994). Temporal discounting and preference reversals in choice between delayed outcomes. Psychonomic Bulletin & Review, 1(3), 383-389.

doi: 10.3758/BF03213979 URL |

| [11] |

Green L., & Myerson J. (2004). A discounting framework for choice with delayed and probabilistic rewards. Psychological Bulletin, 130(5), 769-792.

doi: 10.1037/0033-2909.130.5.769 pmid: 15367080 |

| [12] |

He G. -B., Li S., & Liang Z. -Y. (2018). Behavioral decision-making is nudging China toward the overall revitalization. Acta Psychologica Sinica, 50(8), 803-813.

doi: 10.3724/SP.J.1041.2018.00803 URL |

|

[何贵兵, 李纾, 梁竹苑. (2018). 以小拨大: 行为决策助推社会发展. 心理学报, 50(8), 803-813.]

doi: 10.3724/SP.J.1041.2018.00803 |

|

| [13] | Holm S. (1979). A simple sequentially rejective multiple test procedure. Scandinavian Journal of Statistics, 6, 65-70. |

| [14] |

Huang Y. -N., Jiang C. -M., Liu H. -Z., & Li S. (2023). Toward a coherent understanding of risky, intertemporal, and spatial choices: Evidence from eye-tracking and subjective evaluation. Acta Psychologica Sinica, 55(6), 994-1015.

doi: 10.3724/SP.J.1041.2023.00994 |

|

[黄元娜, 江程铭, 刘洪志, 李纾. (2023). 风险、跨期和空间决策的决策策略共享: 眼动和主观判断的证据. 心理学报, 55(6), 994-1015.]

doi: 10.3724/SP.J.1041.2023.00994 |

|

| [15] | Jiang C. -M. (2013). Mechanism of intertemporal choice: From a perspective of equate-to-differentiate model [Unpublished doctoral dissertation]. University of Chinese Academy of Sciences, Beijing, China. |

| [江程铭. (2013). 跨期选择的心理机制: 基于齐当别的视角 (博士学位论文). 中国科学院大学.] | |

| [16] |

Jiang C. M., Chen L. N., Luo Q., Wang W., Zhou J., & Ma J. T. (2025). The token undermining effect: When and why adding a small reward to a dated outcome makes it less preferred. British Journal of Psychology, 116(2), 386-408.

doi: 10.1111/bjop.v116.2 URL |

| [17] |

Jiang C. -M., Liu H. -Z., Cai X. -H., & Li S. (2016). A process test of priority models of intertemporal choice. Acta Psychologica Sinica, 48(1), 59-72.

doi: 10.3724/SP.J.1041.2016.00059 |

| [江程铭, 刘洪志, 蔡晓红, 李纾. (2016). 跨期选择单维占优模型的过程检验. 心理学报, 48(1), 59-72.] | |

| [18] |

Kahneman D., & Tversky A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), 263-292.

doi: 10.2307/1914185 URL |

| [19] |

Kahneman D., & Tversky A. (1982). The Psychology of Preferences. Scientific American, 246(1), 160-173.

doi: 10.1038/scientificamerican0182-160 URL |

| [20] | Kang L., Kuang Y., Li S., Zheng X., & Du F. (2025). The time-space frame in road signs affects pathfinding driving performance: Results from Bayesian networks. Applied Cognitive Psychology, 39(4), e70094. |

| [21] |

Kim B. K., & Zauberman G. (2009). Perception of anticipatory time in temporal discounting. Journal of Neuroscience, Psychology, and Economics, 2(2), 91-101.

doi: 10.1037/a0017686 URL |

| [22] |

Kuang Y., Huang Y. N., & Li S. (2023). A framing effect of intertemporal and spatial choice. Quarterly Journal of Experimental Psychology, 76(6), 1298-1320.

doi: 10.1177/17470218221113519 URL |

| [23] |

Larrick R. P., & Soll J. B. (2008). The MPG Illusion. Science, 320(5883), 1593-1594.

doi: 10.1126/science.1154983 URL |

| [24] |

Levin I. P., & Gaeth G. J. (1988). How consumers are affected by the framing of attribute information before and after consuming the product. Journal of Consumer Research, 15(3), 374-378.

doi: 10.1086/jcr.1988.15.issue-3 URL |

| [25] |

Levin I. P., Gaeth G. J., Schreiber J., & Lauriola M. (2002). A new look at framing effects: Distribution of effect sizes, individual differences, and independence of types of effects. Organizational Behavior and Human Decision Processes, 88(1), 411-429.

doi: 10.1006/obhd.2001.2983 URL |

| [26] |

Levin I. P., Johnson R. D., & Davis M. L. (1987). How information frame influences risky decisions: Between- subjects and within-subject comparisons. Journal of Economic Psychology, 8(1), 43-54.

doi: 10.1016/0167-4870(87)90005-5 URL |

| [27] |

Levin I. P., Schneider S. L., & Gaeth G. J. (1998). All Frames Are Not Created Equal: A Typology and Critical Analysis of Framing Effects. Organizational Behavior and Human Decision Processes, 76(2), 149-188.

pmid: 9831520 |

| [28] | Li S. (1994). Equate-to-differentiate theory: A coherent bi-choice model across certainty, uncertainty and risk [Unpublished doctorial dissertation]. University of New South Wales, Sydney, Australia. |

| [29] |

Li S. (1998). Can the conditions governing the framing effect be determined? Journal of Economic Psychology, 19(1), 133-153.

doi: 10.1016/S0167-4870(97)00039-1 URL |

| [30] | Li S. (2001). Allais paradox: A behavioral explanation. Acta Psychologica Sinica, 33(2), 176-181. |

| [李纾. (2001). 艾勒悖论(Allais Paradox)另释. 心理学报, 33(2), 176-181.] | |

| [31] | Li S. (2016). An equate-to-differentiate way of decision making (in Chinese). East China Normal University Press. |

| [李纾. (2016). 决策心理: 齐当别之道. 上海: 华东师范大学出版社.] | |

| [32] |

Li S., & Adams A. S. (1995). Is there something more important behind framing? Organizational Behavior and Human Decision Processes. 62(2), 216-219.

doi: 10.1006/obhd.1995.1044 URL |

| [33] | Li S., Fang Y. Q., & Zhang X. J. (2000). What makes frames work? Acta Psychologica Sinica, 32(2), 229-234. |

| [李纾, 房永青, 张迅捷. (2000). 再探框架对风险决策行为的影响. 心理学报. 32(2), 229-234.] | |

| [34] | Li S., & Xie X. (2006). A new look at the “Asian disease” problem: A choice between the best possible outcomes or between the worst possible outcomes? Thinking & Reasoning, 12(2), 129-143. |

| [35] | Li Y., Zhang X., & Chang X. (2015). China's National Balance Sheet 2015: Leverage Adjustment and Risk Management. China Social Sciences Press. |

| [李扬, 张晓晶, 常欣. (2015). 中国国家资产负债表2015:杠杆调整与风险管理. 中国社会科学出版社.] | |

| [36] |

Liu H. Z., Jiang C. M., Rao L. L., & Li S. (2015). Discounting or priority: Which rule dominates the intertemporal choice process? Acta Psychologica Sinica, 47(4), 522-532.

doi: 10.3724/SP.J.1041.2015.00522 |

| [刘洪志, 江程铭, 饶俪琳, 李纾. (2015). “时间折扣”还是 “单维占优”?——跨期决策的心理机制. 心理学报. 47(4), 522-532.] | |

| [37] |

Liu H. -Z., Li S., & Rao L. -L. (2018). Out of debt, out of burden: The physical burdens of debt. Journal of Experimental Social Psychology, 76, 155-160.

doi: 10.1016/j.jesp.2018.01.003 URL |

| [38] |

Loewenstein G., & Prelec D. (1992). Anomalies in intertemporal choice: Evidence and an interpretation. Quarterly Journal of Economics, 107(2), 573-597.

doi: 10.2307/2118482 URL |

| [39] |

Luckman A., Donkin C., & Newell B. (2020). An evaluation and comparison of models of risky intertemporal choice. Psychological Review, 127(6), 1097-1138.

doi: 10.1037/rev0000223 URL |

| [40] | Luo X., Liang Q., & Yang X. (2017). “Gray Rhino” and “Black Swan” for current China’s economy. Bulletin of Chinese Academy of Sciences, 32(12), 1356-1370. |

| [骆晓强, 梁权琦, 杨晓光. (2017). 当前中国经济的“灰犀牛”和“黑天鹅”. 中国科学院院刊, 32(12), 1356-1370.] | |

| [41] | Ma J. T. (2025). Dual modes of temporal decision-making: Cross-period and cross-point decision-making [Unpublished Doctoral dissertation]. Zhejiang University, Hangzhou, China. |

| [马家涛. (2025). 时间决策的双模式:跨时间段和跨时间点决策的行为特点与心理机制 (博士学位论文). 浙江大学.] | |

| [42] | Ma J. T., He G. B., & Li S. (2023). A Study on cross-period temporal choice and Its Mechanisms: Different from cross-point temporal choice. The 4rd Annual Conference of Decision Making Psychology Professional Committee of Chinese Psychological Society. Xinjiang, China. |

| [马家涛, 何贵兵, 李纾. (2023). 有别于点跨期决策的段跨期决策及其机制初探. 中国心理学会决策心理学专业委员会第四届学术年会. 新疆喀什.] | |

| [43] | Ma J. T., He G. B., & Li S. (2024). Which decision - temporal decision via the trade-off between "earlier vs. later" or via the trade-off between "shorter vs. longer" - can explain and predict people's far-sighted behavior? The 5rd Annual Conference of Decision Making Psychology Professional Committee of Chinese Psychological Society. Tibet, China. |

| [马家涛, 何贵兵, 李纾. (2024). 权衡“迟早”的时间决策与权衡“长短”的时间决策, 哪种决策能解释和预测人们的远视行为?. 中国心理学会决策心理学专业委员会第五届学术年会. 西藏林芝.] | |

| [44] | Ma J. T., Wang L., Chen L. N., He Q., Sun Q. Z., Sun H. Y., & Jiang C. M. (2021). Comparing mixed intertemporal tradeoffs with pure gains or pure losses. Judgment and Decision Making, 16(3), 709-728. |

| [45] |

Nan L. X., Park S., & Yang Y. (2023). Rejections are more contagious than choices: How another’s decisions shape our own. Journal of Consumer Research, 50(2), 363-381.

doi: 10.1093/jcr/ucad007 URL |

| [46] | Qiu Z., Wang Z., & Wang Z. (2022). Local government debt replacement plan and new implicit debt——Based on issuance scale and pricing of chengtou bonds. China Industrial Economics, 4, 42-60. |

| [邱志刚, 王子悦, 王卓. (2022). 地方政府债务置换与新增隐性债务——基于城投债发行规模与定价的分析. 中国工业经济, 4, 42-60.] | |

| [47] |

Read D., Frederick S., Orsel B., & Rahman J. (2005). Four score and seven years from now: The date/delay effect in temporal discounting. Management Science, 51(9), 1326-1335.

doi: 10.1287/mnsc.1050.0412 URL |

| [48] |

Shen S. C., Khishignyam B., Ding Y., Ma J. T., Yang S. W., Kuang Y., … Li S. (2023). Changes in the intertemporal choices of people in or close to Chinese culture can predict their self-rated survival achievement in the fight against COVID-19: A cross-national study in 18 Asian, African, European, American, and Oceanian countries. Acta Psychologica Sinica, 55(3), 435-454.

doi: 10.3724/SP.J.1041.2023.00435 |

|

[沈丝楚, 希喜格, 丁阳, 马家涛, 杨舒雯, 匡仪, … 李纾. (2023). 跨期选择的变易程度正向预测中华文化圈国民的自评扛疫成效:亚非欧美大洋洲18国跨国研究. 心理学报, 55(3), 435-454.]

doi: 10.3724/SP.J.1041.2023.00435 |

|

| [49] |

Shen S. C., Wang Y. M., Zhang H. B., & Ma J. T. (2023). Discount or trade off: The psychological mechanisms of intertemporal choice with double-dated mixed outcomes. Advances in Psychological Science, 31(7), 1121-1132.

doi: 10.3724/SP.J.1042.2023.01121 URL |

|

[沈丝楚, 王耀民, 张寒冰, 马家涛. (2023). 折扣还是权衡:混合得失双结果跨期决策的理论探索. 心理科学进展, 31(7), 1121-1132.]

doi: 10.3724/SP.J.1042.2023.01121 |

|

| [50] | Stanovich K. E., & West R. F. (1998). Individual differences in framing and conjunction effects. Thinking & Reasoning, 4(4), 289-317. |

| [51] |

Sun H. L., Li A. M., Shen S. C., Xiong G. X., Rao L. L., Zheng R., Sun H.Y., & Li S. (2020). Early departure, early revival: A "free from care" account of negative temporal discounting. Advances in Cognitive Psychology, 16(2), 103-116.

doi: 10.5709/acp-0289-0 URL |

| [52] | Sun H. -Y., Li A. -M., Chen S., Zhao D., Rao L. -L., Liang Z. -Y., & Li S. (2015). Pain now or later: An outgrowth account of pain-minimization. PLoS ONE. 10(3), e0119320. |

| [53] |

Sun H. -Y., Ma J. -T., Zhou L., Jiang C. -M., & Li S. (2022). Waiting is painful: The impact of anticipated dread on negative discounting in the loss domain. Judgment and Decision Making, 17(6), 1353-1378.

doi: 10.1017/S1930297500009451 URL |

| [54] |

Sun Y., Huang L., & Liu Y. (2012). Graph-framing effects in decision making. Advances in Psychological Science, 20(11), 1718-1726.

doi: 10.3724/SP.J.1042.2012.01718 |

|

[孙彦, 黄莉, 刘扬. (2012). 决策中的图形框架效应. 心理科学进展, 20(11), 1718-1726.]

doi: 10.3724/SP.J.1042.2012.01718 |

|

| [55] |

Sun Y., Li S., Bonini N., & Su Y. (2012). Graph framing effects in decision making. Journal of Behavioral Decision Making. 25(5), 491-501.

doi: 10.1002/bdm.v25.5 URL |

| [56] | Sunstein C. R. (2014). Why nudge?: The politics of libertarian paternalism. Yale University Press. |

| [57] |

Tang S., Koval C. Z., Larrick R. P., & Harris L. (2020). The morality of organization versus organized members: Organizations are attributed more control and responsibility for negative outcomes than are equivalent members. Journal of Personality and Social Psychology, 119(4), 901-919.

doi: 10.1037/pspi0000229 pmid: 32105101 |

| [58] |

Thaler R. (2021). What’s next for nudging and choice architecture? Organizational Behavior and Human Decision Processes, 163, 4-5.

doi: 10.1016/j.obhdp.2020.04.003 URL |

| [59] | Thaler R. H., & Sunstein C. R. (2008). Nudge: Improving decisions about health, wealth, and happiness. New Haven, CT: Yale University Press. |

| [60] |

Tversky A., & Kahneman D. (1981). The framing of decisions and the psychology of choice. Science, 211(4481), 453-458.

doi: 10.1126/science.7455683 pmid: 7455683 |

| [61] |

Tversky A., & Kahneman D. (1992). Advances in prospect theory: Cumulative representation of uncertainty. Journal of Risk and Uncertainty, 5(4), 297-323.

doi: 10.1007/BF00122574 URL |

| [62] |

Wang Z., Chen C., Mo J., Lu F., Ma J. T., Chen C., & He G. (2023). Experiencing Buddhist practices promotes nonbelievers’ preference for future rewards in intertemporal choices. European Journal of Social Psychology, 53(1), 230-244.

doi: 10.1002/ejsp.v53.1 URL |

| [63] | Xu L. J., Liang Z. Y., Wang K., Li S., & Jiang T. Z. (2009). From discounting future gains to future losses. China Basic Science, 11(6), 25-27. |

| [徐丽娟, 梁竹苑, 王坤, 李纾, 蒋田仔. (2009). 跨期选择的神经机制:从折扣未来获益到折扣未来损失. 中国基础科学, 11(6), 25-27.] | |

| [64] |

Zauberman G., Kim B. K., Malkoc S. A., & Bettman J. R. (2009). Discounting time and time discounting: Subjective time perception and intertemporal preferences. Journal of Marketing Research, 46(4), 543-556.

doi: 10.1509/jmkr.46.4.543 URL |

| [65] | Zhang K. (2016). Column call for papers: Behavioral decision-making is nudging China toward the overall revitalization. Acta Psychologica Sinica. https://journal.psych.ac.cn/xlxb/CN/news/news13.shtml |

| [张侃. (2016). “以小拨大: 行为决策助推社会发展”专栏征稿启事. 心理学报. https://journal.psych.ac.cn/xlxb/CN/news/news13.shtml] | |

| [66] | Zhang S., & Li S. (2018). Exploring behavioral public administration: Content, method and trend. Journal of Public Administration, 11(1), 1-36+219. |

| [张书维, 李纾. (2018). 行为公共管理学探新: 内容、方法与趋势. 公共行政评论, 11(1), 1-36+219.] | |

| [67] | Zhang Y. -Y., Zhou L., Li S., & Liang Z. -Y. (2022). Computation of subjective value does not always elicit alternative-based information searching in intertemporal choice. Journal of Behavioral Decision Making, 35(4), 1-13. |

| [68] | Zhang Y. Y., Zhou L., You X. Q., Li S., & Liang Z. Y. (2018). Is intertemporal decision-making based on a temporal discounting process? Evidence from doubledissociation paradigm. Scientia Sinica (Vitae), 48(5), 592-608. |

| [张阳阳, 周蕾, 游旭群, 李纾, 梁竹苑. (2018). 跨期决策是否基于“折扣计算”: 来自双分离范式的证据. 中国科学:生命科学, 48(5), 592-608.] | |

| [69] |

Zhou L., Li A. M., Zhang L., Li S., & Liang Z. Y. (2019). Similarity in processes of risky choice and intertemporal choice: The case of certainty effect and immediacy effect. Acta Psychologica Sinica, 51(3), 337-352.

doi: 10.3724/SP.J.1041.2019.00337 |

|

[周蕾, 李爱梅, 张磊, 李纾, 梁竹苑. (2019). 风险决策和跨期决策的过程比较: 以确定效应和即刻效应为例. 心理学报, 51(3), 337-352.]

doi: 10.3724/SP.J.1041.2019.00337 |

|

| [70] |

Zhou L., Yang Y., & Li S. (2022). Music-induced emotions influence intertemporal decision making. Cognition and Emotion, 36(2), 211-229.

doi: 10.1080/02699931.2021.1995331 URL |

| [1] | 徐岚, 陈全, 崔楠, 辜红. “共赢” vs. “牺牲”: 道德消费叙述框架对消费者算法推荐信任的影响[J]. 心理学报, 2024, 56(2): 179-193. |

| [2] | 孙庆洲, 黄靖茹, 虞晓芬, 高倾德. 授人以鱼还是授人以渔?高、低社会阶层的捐助行为差异[J]. 心理学报, 2023, 55(10): 1677-1695. |

| [3] | 崔芳, 杨佳苗, 古若雷, 刘洁. 右侧颞顶联合区及道德加工脑网络的功能连接预测社会性框架效应:来自静息态功能磁共振的证据[J]. 心理学报, 2021, 53(1): 55-66. |

| [4] | 刘隽, 张震, 孙彦, 韩布新, 陆勤, 刘萍萍. 接受还是拒绝? 反应模式助推基础课与拓展课均衡选择[J]. 心理学报, 2019, 51(4): 437-449. |

| [5] | Gerd Gigerenzer, 栾胜华, 刘永芳. 人非理性且难教化?论支持自由家长主义的证据[J]. 心理学报, 2019, 51(4): 395-406. |

| [6] | 黄元娜, 宋星云, 邵洋, 李纾, 梁竹苑. 以小拨大:默认选项和反应模式效应助推中国器官捐献登记 *[J]. 心理学报, 2018, 50(8): 868-879. |

| [7] | 李爱梅, 王海侠, 孙海龙, 熊冠星, 杨韶丽. “长计远虑”的助推效应:怀孕与环境跨期决策 *[J]. 心理学报, 2018, 50(8): 858-867. |

| [8] | 王晓庄, 安晓镜, 骆皓爽, 徐晟, 于馨, 胡施雅, 王玉涵. 锚定效应助推国民身心健康:两个现场实验 *[J]. 心理学报, 2018, 50(8): 848-857. |

| [9] | 路西, HSEE. 联合评估和单独评估:富有潜力的助推手段[J]. 心理学报, 2018, 50(8): 827-839. |

| [10] | Nicolao Bonini, Constantinos Hadjichristidis, Michele Graffeo. 绿色助推[J]. 心理学报, 2018, 50(8): 814-826. |

| [11] | 何贵兵, 李纾, 梁竹苑. 以小拨大:行为决策助推社会发展[J]. 心理学报, 2018, 50(8): 803-813. |

| [12] | 马文娟,索涛,李亚丹,罗笠铢,冯廷勇,李红. 得失框架效应的分离—— 来自收益与损失型跨期选择的研究[J]. 心理学报, 2012, 44(8): 1038-1046. |

| [13] | 宋广文,夏星星,李承宗,何云凤. 时间距离、封面故事和概率对框架效应的影响[J]. 心理学报, 2012, 44(7): 957-963. |

| [14] | 贺伟,龙立荣. 薪酬体系框架与考核方式对个人绩效薪酬选择的影响[J]. 心理学报, 2011, 43(10): 1198-1210. |

| [15] | 孙彦,许洁虹,陈向阳. 封面故事、选项框架和损益概率对风险偏好的影响[J]. 心理学报, 2009, 41(03): 189-195. |

| 阅读次数 | ||||||

|

全文 |

|

|||||

|

摘要 |

|

|||||